Late last year, Congress passed the biggest federal tax overhaul in decades, a change which is unofficially referred to as the Tax Cuts and Jobs Act of 2017. Originally intended to simplify tax filings, it did anything but. What do these tax changes mean to individuals with disabilities and their families? The answer depends on where they fall in the tax brackets.

For many individuals and families, the tax savings will be less than had been signaled by Congress and the White House. While individual tax rates dropped slightly and the standard deduction doubled, the personal exemption has been discontinued. Rates for capital gains, qualified dividends and net investment income stayed the same. Many itemized deductions were repealed and those that remain should be weighed against the improved standard deduction, both in terms of actual savings and the increased complexity of the filing process. As a rule of thumb, 2017’s tax changes will prove most beneficial to families with adjusted gross incomes of $60,000 or more.

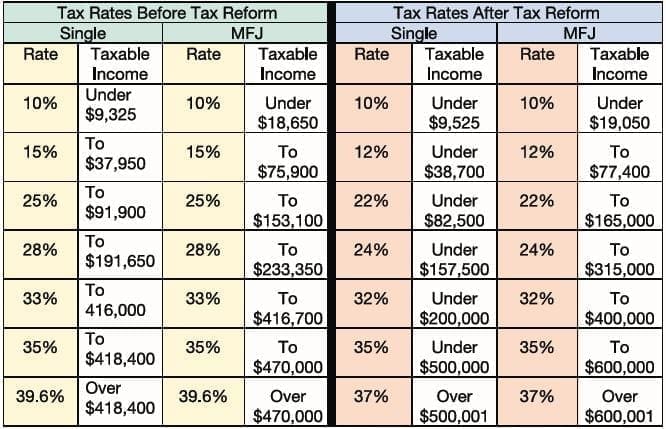

Here is a chart that compares federal tax rates for single individuals and for married individuals filing jointly (“MFJ”) before and after passage of the tax legislation. It illustrates that, in general, individual tax rates dropped two to three percentage points.

In addition, while changes to corporate taxes are permanent, the new personal tax provisions are temporary, requiring congressional action to prevent their expiration in 2025. Lobbying efforts are afoot, and how these provisions may change over time is anyone’s guess. But for purposes of planning for tax year 2018, here are the highlights.

What Stayed the Same

It had been feared that the deduction for medical expenses would disappear, but it remains intact. In fact, for purposes of 2018 taxes, it’s slightly more generous than it was prior to the legislation—applicable to outlays exceeding 7.5 percent of the filer’s adjusted gross income. Beginning in tax year 2019, the 10 percent threshold returns. Individuals whose medical costs are largely covered by Medicare or Medicaid are likely to be challenged to meet this requirement.

Education-related deductions are also unchanged. If there are out-of-pocket costs for schooling at any level, they can be claimed.

Additionally, third-party special needs trusts (SNTs) structured for qualified disability trust (QDisT) treatment continue to enjoy tax-favored status. But the reason that QDisTs receive tax-preferred treatment has changed. Prior to the new law, QDisTs qualified for a larger personal exemption than other tax-paying trusts─ $4,050 versus $100. After tax reform, QDisTs continue to receive a personal exemption, rather than losing it like other taxpayers.

For 2018, the QDisT exemption has actually increased to $4,150. But remember, any distribution from the income of a separately taxable trust to or for the beneficiary becomes taxable to that individual rather than the trust, as long as the distribution doesn’t exceed income received by the trust. The result is that, though the calculation changes, the amount of income which can be completely tax-sheltered continues to be significantly greater if the trust is a QDisT.

You can still deduct contributions to your favorite charity—even if you’re not itemizing. In fact, the limit has been increased for contributions of cash to 60 percent of the filer’s adjusted gross income. If cash donations exceed that threshold, they can be carried forward for up to five tax years.

Other remaining credits and exclusions that may be of special interest to families include:

- The child and dependent care expense credit,

- The adoption credit, and

- The exclusion for employer plan assistance for dependent care and adoption costs.

While the alternative minimum tax remains, its exemptions have been increased.

What Changed

Perhaps the most significant tax change for most families is, as mentioned earlier, the doubling of the standard deduction, which jumps from $12,000 to $24,000 for married couples who file jointly. An additional standard deduction for the blind and elderly remains in place.

The new standard deduction, along with the repeal of personal exemptions (which would otherwise have been $4,150 in 2018), will largely define the new tax landscape for many families─especially since many itemized deductions are no longer available.

One highly publicized modification, which became a bargaining chip during congressional negotiations, was the increase in the child tax credit from $1,000 to $2,000, but only $1,400 of the credit can be paid out if the taxpayer is due a refund. This credit is available to those claiming dependents under 16 and whose adjusted gross income is under $200,000 for single heads of household or $400,000 for married couples filing jointly. An additional nonrefundable credit of $500 is available for other dependents if the dependent has been living with the filer for over six months during the applicable tax year.

There is no longer a penalty for failing to carry health insurance, which was a focal point of the Affordable Care Act (ACA). It does not appear, though, that this change is having much effect on insurance markets. Instead, those markets seem to be more sensitive to other─ non-tax─ regulatory actions.

Itemized Deductions

There’s been lots of controversy over the scaling back of the deduction for state and local taxes. As of the 2018 tax year, non-corporate filers may deduct no more than $10,000 of the state and local property and income taxes paid. This hits hard in states with high taxes and property costs, and various workarounds are being proposed by state legislators. In August, the IRS issued proposed regulations blocking those efforts.

The miscellaneous itemized expenses of a trust are no longer deductible, a change which will affect both special needs and traditional trusts alike. The most obvious lost deductions are for investment and tax filing fees. On the other hand, trustee fees are still deductible.

The deduction for mortgage interest, while grandfathered, is scaled back for loans made after January 1, 2018. The new deduction is limited to interest charged on a principal of $750,000. In addition, the interest on home equity loans is no longer deductible.

The financial implications of divorce [1] have become more complicated, beginning in tax year 2019. Through tax year 2018, the spouse paying alimony can deduct it, with the recipient being required to treat alimony received as income. As of tax year 2019, however, the tax burden shifts. The spouse who pays alimony is liable for tax on the full amount, while the other party receives the alimony tax-free. If contemplating a divorce, parents should carefully consider the tax implications as they negotiate the financial terms which will apply.

In addition, there is no longer a deduction for casualty and theft losses.

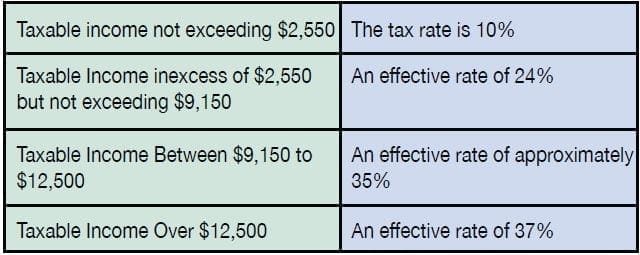

Dependent’s Unearned Income

A dependent’s net unearned income will now be taxed at the highest rate applied to estates and trusts, not the parents’ highest rates, all as follows:

QDisT distributions continue to be exempt from the rules on how the unearned income of a dependent is taxed.

Specialized Savings Accounts

ABLE accounts, which are cousins of 529 education savings accounts, are state-defined savings tools for individuals whose disability appeared prior to age 26. The tax advantage available with both ABLE and 529 Plans is that the return on investment in each is received tax-free as long as the funds are used for qualifying expenses─education costs for 529 accounts and certain disability expenses for ABLE accounts. The 2017 Tax Act affects both:

- Distributions from 529 accounts may now be used to pay for education costs related to kindergarten through high school, up to $10,000 annually.

- Funds held by a 529 account established for a child with disabilities who will not attend college can be rolled into an ABLE account up to the annual limit for ABLE Accounts ($15,000 in 2018). For example, it will take two years to transfer a $30,000 529 account to an ABLE Account.

- Rollovers to ABLE accounts from 529 accounts of other family members who won’t be using them are now allowed, up to the $15,000 annual contribution cap. The transfer must be made within 60 days of determining that the fund won’t be used for school expenses.

- An ABLE beneficiary may now contribute their own earnings to ABLE accounts on top of the $15,000 annual limit. To qualify, their total earnings must be below the federal poverty limit ($12,060 for a single individual in 2018) and they cannot be a participant in an employer retirement plan.

- ABLE beneficiaries making contributions to their own accounts are eligible for a savings credit up to $1,000 if they are low-income taxpayers.

Related: Able Accounts and Taxes: What Special Needs Families Need to Know [2]

Entrepreneurs

Entrepreneurs and self-employed individuals may be eligible for an especially generous benefit, a deduction allowing qualifying business owners to deduct up to 20 percent of their net business income. Known as the qualified business income deduction, it is available, under certain circumstances, to businesses for which profits are taxed on the returns of its owner(s), a list which includes sole proprietorships, partnerships, S corporations and LLCs.

But the calculation can be tricky, and owners will need to assess whether they should pay a tax professional to assist them. During tax year 2018, the deduction is available to individuals with adjusted gross income less than $157,500 ($315,000 for joint filers).

Related: Person-Ventured Entrepreneurship: What Do You Know About Entrepreneurship [3]

The Upshot

The takeaway from all this? Federal tax policy is as complicated as ever, and families should consult their financial advisors to ensure that they understand its implications for their specific circumstances. Filers at higher income levels are likely to benefit the most from these changes since, for many working families, the potential savings from itemizing won’t justify the complexity and cost of working through the details. For them, taking the improved standard deduction is likely to be the best bet.![]()

James M. McCarten, Esq, is a partner in the tax, trusts, estates and corporate practice groups of Burr & Forman, Atlanta, Georgia and Nashville, Tennessee. He is a member of the Special Needs Alliance [4], a national organization comprised of attorneys committed to assisting individuals with disabilities, their families and the professionals who serve them.

Helpful Articles

- Financial Planning: For Those Who Are at the Starting Line [5]

- Special Needs Financial Planning During COVID [6]

- Guardianship: A Basic Understanding for Parents [7]

- An Affordable Proposal for Guardianship: The Special Needs Tax Credit Bill [8]

- 9 Things You Need to Know to Maximize Your Child’s Benefits [9]

- Social Security Benefits: Understanding How To Work? [10]

- Applying for SSI Benefits for a Child With Special Needs [11]

- Does Your Child Qualify for Supplemental Security Income? Dispelling Misconceptions [12]

- Special Needs Planning: What is a Special Needs Trust? [13]

- “Instruction Manual” for Your Child with Special Needs [14]

- Common Mistakes Parents Make with Their Special Needs Trusts [15]

- Tax Planning for Parents of Children with Autism [16]

- Able Account or Special Needs Trust: How to Decide? [17]

- Special Needs Planning: What is a Special Needs Trust? [13]

- Special Needs (or Supplemental Needs) Trusts 101 [18]

- Able Accounts and Taxes: What Special Needs Families Need to Know [2]

- ABLE Accounts: 10 Things You Should Know [19]

- How to Select a Special Needs Attorney [20]

This post originally appeared on our January/February 2019 Magazine [21]