Able Account or Special Needs Trust

In December 2014, President Obama signed the Stephen Beck Jr. Achieving a Better Life Experience Act (“ABLE Act”) into law, authorizing states to create a new category of savings programs for certain individuals with disabilities. Assets held in accounts that comply with the ABLE Act will not affect eligibility for Medicaid or Supplemental Security Income (“SSI”), so long as they are used for “qualified disability-related purposes.” In planning for the future security of a child with special needs, many families wonder how ABLE accounts differ from special needs trusts (SNTs), which also safeguard a beneficiary’s public benefits. When should they establish one versus the other? The choice depends on personal circumstances, and in some cases, it may make sense to create both an ABLE account and an SNT.

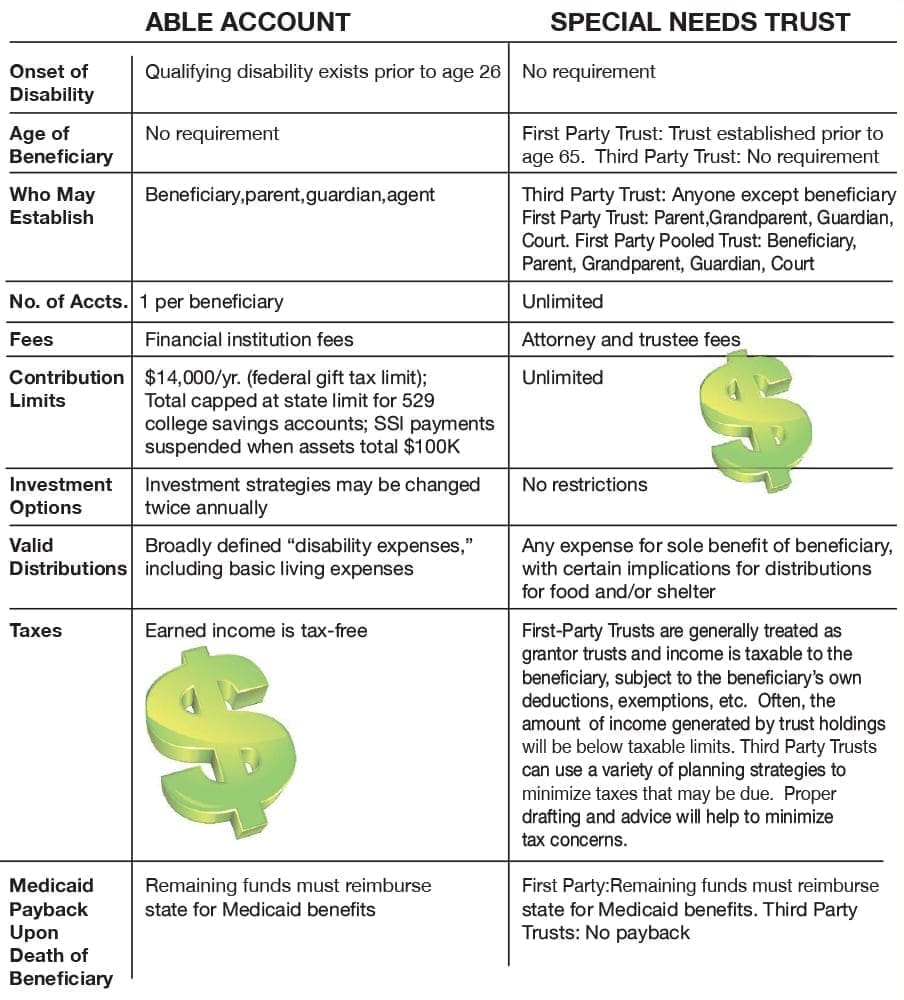

ABLE legislation has been passed or is pending in 41 states. Implementation, however, will await final federal and state regulations, including regulations from the Internal Revenue Service. The Social Security Administration recently published new guidelines for ABLE Accounts in the Program Operations Manual System (POMS), but as with all developing programs, more specific implications will likely develop over time.. Accounts in some states are expected to begin to be available in the future. While some specifics will vary by state, the major distinctions between ABLE accounts and SNTs are:

Sorting It Out

Clearly there are real differences between ABLE accounts and SNTs. For someone whose disability appears at the age of 26 or later, ABLE is not an option. Neither is it feasible for handling inheritances or personal injury settlements that exceed $14,000 (for 2015 and 2016). On the other hand, for families wishing to save no more than $14,000 annually or $100,000 in total, ABLE accounts may prove extremely useful. Trusts limit the beneficiary’s control, giving all decision making authority with regard to distributions to the trustee. The independence that an ABLE account makes possible for the beneficiary may be invaluable.

The IRS has signaled that valid ABLE account distributions will be broadly defined, including basic living expenses. SNT distributions, however, may be used for virtually anything intended for the beneficiary’s sole benefit. SNT funds can pay for a vacation, a concert or a computer game without affecting eligibility for means-tested benefits. Families should carefully consider their planning objectives before making a choice.

It may be beneficial to have both types of accounts

ABLE accounts are less expensive to establish than an SNT, but their Medicaid payback requirement may be an important consideration if parents have other heirs they wish to receive remaining assets upon the beneficiary’s death.

In some cases, it may be beneficial to have both an ABLE account and a SNT. Beneficiaries wishing to “spend down” assets below SSI’s (Supplemental Security Income) $2,000 limit could place those funds in an ABLE account for easy access, while larger amounts could be allocated to a SNT.

In June of 2015, the IRS issued proposed regulations that many advocacy organizations criticized as too administratively burdensome. In response, the government has announced interim guidelines addressing some of those concerns. In addition to simplified reporting requirements, the IRS has indicated that if an ABLE beneficiary overcomes their disability, beginning on the first day of the next tax year, no contributions may be accepted to the ABLE account, although it remains otherwise intact. If the individual’s eligibility is subsequently reinstated, additional contributions may be accepted.

Questions still remain

Final IRS regulations, are pending, and a number of important concerns remain unaddressed. Even with the Social Security Administration’s recent publication of specific POMS, some questions and policy details remain. For instance, when someone is unable to establish an ABLE account on their own, the federal guidelines indicate that the only persons who may do so on their behalf are their agent under a power of attorney, a legal guardian or parent. This may be overly restrictive and could leave some individuals without recourse. If questions such as this are not laid to rest by the final regulations, it may fall to the courts to determine answers.

ABLE accounts are an exciting new tool with considerable potential to add flexibility to a comprehensive special needs plan.![]()

Scott C. Suzuki, Esq., is president of the Special Needs Alliance, SNA, a national nonprofit comprised of attorneys who assist individuals with disabilities, their families and the professionals who serve them.

Helpful Articles

- Able Accounts and Taxes: What Special Needs Families Need to Know [1]

- “Instruction Manual” for Your Child with Special Needs [2]

- ABLE Accounts: 10 Things You Should Know [3]

- Guardianship: A Basic Understanding for Parents [4]

- Handling Your Child’s Diagnosis: Six Things Parents Should Do For Themselves [5]

- A Special Need Planning Timeline: 9 Steps to a Sound Family Plan [6]

- Plan Early for Your Child’s Long-Term Security [7]

- Able Account or Special Needs Trust: How to Decide? [8]

- Special Needs Planning: What is a Special Needs Trust? [9]

- Special Needs (or Supplemental Needs) Trusts 101 [10]

- Common Mistakes Parents Make with Their Special Needs Trusts [11]

This post originally appeared on our January/February 2016 Magazine [12]