Beth C. Manes, Esq., Explains Able Accounts to Empower Special Needs Families

Parents often ask for advice on what to do with the assets owned by their adult children with disabilities. Should they open an ABLE account? Should they have a special needs trust? Or, should they have both? As with most questions posed to lawyers, the answer is: it depends. First, it is important to understand the differences among ABLE accounts and the variations of special needs trust (“SNTs”). Then, clients can evaluate which vehicle, or vehicles, best achieve their family’s goals.

“Able Accounts are to disability expenses as 529s are to education expenses.” ~Beth Manus

NAVIGATING SPECIAL NEEDS PLANNING: ABLE ACCOUNTS VS. SPECIAL NEEDS TRUSTS

What is an ABLE account?

In 2014, Congress passed the Achieving a Better Life Experience Act. This legislation created tax-advantaged savings accounts for people with disabilities, known as ABLE accounts.

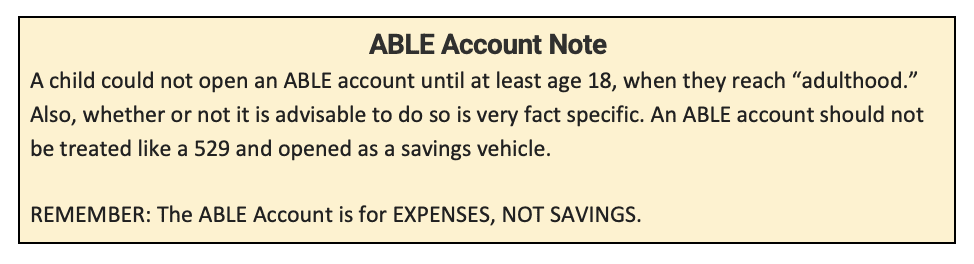

Currently, the ABLE Act limits eligibility to individuals with disabilities with an age of onset of disability prior to reaching age 26, but that qualifying age will increase to 46 on January 1, 2026. The qualifying disability must have lasted, or be expected to last, for at least 12 months or result in death. Finally, the individual must meet Social Security’s criteria regarding significant functional limitations stemming from the disabling condition.

ABLE Account Rules and Limits

An ABLE account can be funded with the person’s own funds (i.e., a UTMA account, inheritance, award or settlement funds from a personal injury lawsuit, child support), or with funds from other people. However, once money is in an ABLE account, it is considered an asset of the account holder, who is the person with a disability. Therefore, if any funds remain in the account at the time the individual dies, Medicaid is entitled to be paid back before those funds go into the person’s estate to be distributed to their beneficiaries or next of kin.

Control and Usage of ABLE Funds

ABLE accounts can be used to pay for “qualified disability expenses” (“QDE”), which include anything that helps a person with a disability improve health, independence, or quality of life. QDEs can include basic costs of living, as well as costs for education, food, employment, transportation, technology, support services, and more.

In 2024, an individual cannot put more than $18,000 per year into an ABLE account (this amount is linked to the annual gift amount permitted under the Internal Revenue Code (“IRC”). There are also two “account total” limits to keep in mind. The first is tied to the 529 Plan (tax-advantaged education savings plan) limits, and in New Jersey is $305,000. The second is a federal limit of $100,000, which cannot be exceeded if the beneficiary is receiving Supplemental Security Income (“SSI”).

The money in an ABLE account is controlled by the account holder, or that person’s guardian. The funds can be accessed via on-line transfers or payments, use of a debit/credit card, or mail-in forms. Alternatively, the account holder or guardian can call the ABLE account administrator to make transfers or payments.

What is Special Needs Trust?

A special needs trust, sometimes referred to as a supplemental needs trust, is a trust established for a person with special needs. It is intended to supplement, not supplant, any funds or services the person with special needs may receive from government programs. There are several types of special needs trusts; the SNTs most frequently used in conjunction with, and compared to, an ABLE account are a self-settled trust and a third-party trust. Those trusts are defined by how they are funded, and the money in the trusts is treated differently for the same reason.

Types of Special Needs Trusts

Self-settled Trust:

A self-settled trust is funded with the beneficiary’s own money (i.e., a UTMA account, inheritance, award or settlement funds from a personal injury lawsuit, child support). Therefore, like an ABLE account, there is a pay-back provision. It is also important to note that any payments over $5,000 must be approved by Medicaid.

Third-Party Trust:

A third-party trust is funded with someone else’s money (i.e., gifts made to the trust, an inheritance directed into the trust). Since this is money that never goes through the individual’s hands, and cannot be considered that person’s money, there is no payback provision and the creator of the trust can choose the ultimate beneficiaries who will receive the remaining assets of the trust after the person with a disability dies.

Differences in Trust Funding and Control

Unlike with an ABLE account, there is no contribution limit to a special needs trust, other than the gift limitations regulated by the IRC. Funds in an SNT are controlled by the trustee. The trustee can be either an individual or an institutional trustee, but the trustee of the SNT cannot be the beneficiary, or the beneficiary’s spouse. Although an institutional trustee will charge a fee, it is often worth the cost to have a professional who is familiar with the regulations governing SNTs administering the trust. Further, it is also often better for the family dynamic to have an independent person or entity in control of the purse strings of the person with a disability rather than a sibling.

Comparing ABLE Accounts and Special Needs Trusts

Which is better? Determining whether a special needs trust (and if so, which type) or an ABLE account is appropriate will be very fact-specific. Many factors need to be considered before a decision is made. Generally, SNTs are suitable for larger assets and offer more flexibility (and third-party trusts are more flexible than self-settled trusts), while ABLE accounts are designed for individuals with disabilities to save smaller amounts without affecting government benefits.

Determining Suitability: Factors to Consider

Additionally, the cost of establishing an ABLE account is lower than that for a trust. Families must first consider the source of the assets that will be used to open and continue to fund the account or trust. After that, it is important to consider the individual who will need the money, how much control over the money is appropriate, what expenses will need to be covered, and how are services (including housing and health care) being provided, both now and in the future. Families should consult with a legal professional to assess their needs and create a plan tailored to their circumstances.

Reach Out for Special Needs Planning Assistance

If you have questions about which vehicle is best for your family, or have any other special needs planning questions, please reach out to Manes & Weinberg, LLC [1], to discuss your family’s needs and options.

[2]

[2]

You May Also Like

- Financial Planning: For Those Who Are at the Starting Line [3]

- Able Accounts and Taxes: What Special Needs Families Need to Know [2]

- Able Account or Special Needs Trust: How to Decide? [4]

- Able Accounts: 10 Things You Should Know [5]

- Have You heard? IRS Increases Limit For ABLE Accounts [6]

This post originally appeared on our January/February 2024 Magazine [7]